The Integrated-Fashion Ecosystem A Macro Analysis

The fashion ecosystem is no longer a linear ‘factory-to-closet’ model. It has evolved into something far more complex, a hyper-connected network where textile manufacturing, digital retail, cultural influence, personal care, and AI-driven forecasting all converge in real time. The sheer scale of this system is staggering: by 2026, the global fashion industry is estimated to exceed $3 trillion in total economic value, encompassing everything from raw cotton cultivation to luxury resale platforms operating in over 80 countries.

Despite the buzz surrounding its digital transformation, the industry remains, in many respects, stubbornly analog. According to McKinsey’s State of Fashion report, most apparel brands invest only 3–5% of revenue into technology, a fraction of what peer industries like financial services or retail electronics spend. The result is a sector perpetually caught between its artisan heritage and the algorithmic demands of the modern consumer.

To understand fashion in 2026 is to understand what analysts now call Total Fashion Integration, the simultaneous management of physical goods, digital identities, cultural storytelling, and circular supply chains. This report examines each layer of that system, from the creative engine of design and manufacturing to the emerging ‘Phygital’ frontier where your digital avatar’s wardrobe is as commercially valuable as the clothes in your physical closet.

The Fashion Ecosystem: A Macro View

Fashion is one of the few industries that simultaneously touches agriculture, chemistry, logistics, media, and technology, all in the service of something as personal as what we choose to wear. In 2026, the ecosystem can be understood through three primary pillars, each of which circulates not just money, but data, cultural meaning, and aesthetic value.

The Fashion Ecosystem: A Macro View

Design & Manufacturing: The Creative Engine

This is where fashion begins. From the hand-stitched precision of Parisian Haute Couture to the algorithm-assisted speed of ultra-fast fashion labels turning trends around in under a week, design and manufacturing form the bedrock of the entire industry. The raw materials involved span natural fibres like cotton, wool, and silk, alongside an expanding range of synthetic and bio-engineered textiles, including lab-grown leather and mycelium-based alternatives that have moved from concept to commercial production in the past two years.

The manufacturing side, however, remains one of fashion’s most persistent challenges. Despite heavy investment in automation and AI-assisted design tools, the physical construction of garments is still overwhelmingly human labour. The International Labour Organization estimates that the global fashion supply chain employs over 75 million people, the majority of them women in Southeast Asia and Sub-Saharan Africa. Automation can cut a pattern and optimise a supply route, but it cannot yet replace the hands that sew a seam at scale, at least not economically.

Retail & Distribution: The Physical Bridge

For decades, the flagship store was fashion’s most powerful asset, a controlled theatrical environment designed to seduce and convert. That model has not died, but it has fundamentally transformed. In 2026, physical retail locations are increasingly positioned as ‘Experience Centers’: spaces designed for immersive brand storytelling, personalised styling appointments, and social-media-ready moments rather than simple inventory off-take. Brands like Loewe, Jacquemus, and Selfridges have pioneered this shift, investing heavily in in-store aesthetics while reducing per-square-foot stock levels.

Online, the distribution landscape is bifurcated. At the mass-market level, Amazon, Tmall, and Alibaba’s combined fashion GMV exceeds $200 billion annually. At the premium end, curated platforms like Net-a-Porter and Mytheresa compete fiercely on editorial identity and service quality, having largely absorbed the market share once held by the now-restructured Farfetch. The disruptors, however, are the re-commerce platforms. The RealReal, Vestiaire Collective, and Depop have moved from niche alternatives to essential infrastructure, serving as both resale marketplaces and authentication authorities in a growing circular economy.

Media & Influence: The Visibility Layer

Visibility, in fashion, is everything. The industry spends an estimated $25 billion annually on marketing and communications, a figure that has shifted dramatically from traditional print advertising toward social media, influencer partnerships, and AI-driven content personalisation. TikTok and Instagram remain the dominant platforms for trend creation and product discovery, with TikTok Shop in particular collapsing the distance between content and commerce. Consumers can now move from first exposure to completed purchase in under 90 seconds, a dynamic that traditional retail and publishing have yet to fully absorb.

Meanwhile, legacy media institutions like Vogue and Harper’s Bazaar continue to hold cultural authority disproportionate to their print circulations, largely because of the credibility they lend to brand campaigns and the roster of photographers, stylists, and critics they sustain. AI-driven trend forecasting tools, offered by companies like WGSN and Trendalytics, now allow brands to predict consumer demand with increasing accuracy months in advance, compressing the traditional trend cycle and rewarding those who act on data as readily as they act on instinct.

Core Product Verticals: Where the Growth Lives

While apparel remains the financial foundation of the global fashion industry, accounting for roughly $1.5 trillion of total market value, the high-margin growth story of 2026 is being written in the satellite categories: cosmetics, fragrance, watches, and accessories. These verticals benefit from lower production costs, higher purchase frequency and a powerful psychological function as ‘entry points’ into luxury ecosystems that would otherwise be inaccessible to most consumers.

| Vertical | 2026 Trend Focus | Market Character |

| Apparel | ‘Quiet Luxury’ & Gender-Neutral | The essential foundation; focus on quality over quantity |

| Cosmetics | Clean Beauty & ‘Glass Skin’ | High frequency, high loyalty; inclusive foundation ranges |

| Watches | Heritage Mechanical vs. High-Tech | A split between Rolex/Patek heirlooms and Apple wearables |

| Perfumes | Niche ‘Storytelling’ Scents | Move toward genderless, artistic fragrances (Le Labo, Byredo) |

| Accessories | Tech-integrated Jewellery | ‘It’ bags and statement eyewear remain the primary luxury entry points |

The cosmetics vertical in particular has undergone a quiet revolution. The ‘glass skin’ aesthetic, inspired by Korean beauty routines and emphasising radiance and transparency over coverage, has driven a structural shift in product formulation and consumer expectation. Clean beauty certifications, once a niche concern, are now table stakes for any brand entering the mass-premium segment. The global cosmetics market is valued at approximately $380 billion in 2026, with skincare representing its fastest-growing sub-category.

In fragrance, the most significant shift is cultural rather than chemical. The dominance of celebrity-licensed scents has given way to an emerging appetite for narrative-driven, ‘niche’ perfume houses. Brands like Byredo, Maison Francis Kurkdjian, and Frederic Malle have built loyal global followings not through mass distribution but through deliberate scarcity and the cultivation of an almost literary identity around each scent. This approach is being rapidly adopted by larger luxury conglomerates, who have recognised that emotional storytelling drives long-term brand equity in a way that traditional advertising cannot.

The Corporate Titans

At the apex of the fashion industry sit a small number of corporate conglomerates that have, over the past three decades, assembled portfolios spanning every segment of the luxury ecosystem. Their dominance is not merely commercial — it is cultural. They set the conditions under which trends emerge, dictate which designers receive global platforms, and increasingly, determine what ‘luxury’ itself means.

LVMH and Kering remain the undisputed twin titans. LVMH, home to Louis Vuitton, Dior, Fendi, Givenchy, Loewe, and Sephora, among dozens of others — reported revenues of approximately €86 billion in 2025, making it the largest luxury goods company in the world by a considerable margin. Kering, steward of Gucci, Saint Laurent, Bottega Veneta, and Balenciaga, has spent recent years navigating a complex repositioning of its flagship Gucci brand following a period of over-exposure, a cautionary tale about the fragility of ‘it’ status in the digital age.

At the opposite end of the value spectrum, Inditex (parent of Zara) and the H&M Group remain masters of mass-market logistics, their competitive advantage rooted in supply chain velocity rather than creative prestige. Both face intensifying pressure from ultra-fast fashion competitors, most notably Shein, which leverages AI-driven demand forecasting to identify microtrends and move from design to delivery in as few as three days. Specialty digital retailers like Net-a-Porter and Mytheresa continue to define the curated luxury e-commerce experience, differentiating themselves through editorial authority and customer service in a landscape where pure product access is increasingly commoditised.

Traffic Drivers: Capturing the Cultural Current

In 2026, organic search traffic in fashion is driven less by product need and more by cultural participation. Consumers do not simply search for ‘a white shirt’, they search for ‘the shirt worn in that Paris café photo’ or ‘the perfect holiday capsule wardrobe for slow travel.’ The shift from keyword-based to vibe-based and intent-based search has profound implications for how brands structure their content, their SEO strategies and their relationship with trend culture.

The ‘dupe’ economy represents one of the largest organic search verticals in the industry. Affordable alternatives to luxury products, particularly in cosmetics, fragrance and accessories, generate enormous search volume, and an entire ecosystem of content creators, comparison platforms and affiliate publishers has grown up to serve that demand. Far from undermining luxury brands, the dupe economy often functions as free advertising, keeping aspirational products in constant cultural conversation.

Drop culture, pioneered by streetwear labels and now adopted by luxury houses, continues to generate some of the most concentrated spikes in search traffic seen anywhere in retail. Limited-edition collaborations, Nike x Jacquemus, New Balance x Aimé Leon Dore, Uniqlo x Marimekko, create a sense of urgency and shared cultural moment that standard product launches cannot replicate. The resale premium attached to successful drops routinely reaches 200–400% of retail price, turning fashion into a form of speculative asset class for a growing segment of younger consumers.

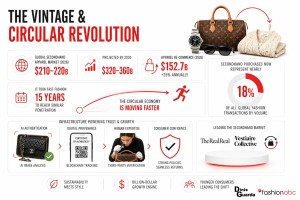

The Vintage & Circular Revolution

The secondhand and vintage market has undergone a transformation in status that would have been difficult to predict a decade ago. What was once the domain of charity shops, niche collectors, and students on tight budgets is now a global economic engine growing at roughly three times the rate of primary fashion retail. The shift is cultural as much as commercial: buying secondhand has acquired genuine social cachet, particularly among younger consumers for whom sustainability credentials and individual style are closely intertwined.

The numbers are striking. The global secondhand apparel market is valued at approximately $210–$220 billion in 2026 and is projected to reach $320–$360 billion by 2030, according to ThredUp’s annual Resale Report.

Apparel re-commerce alone — a subset of the broader secondhand market — is growing at 25% annually and is valued at $152.7 billion this year. Secondhand purchases now represent nearly 18% of all global fashion transactions by volume. For context, it took the fast fashion model fifteen years to achieve comparable market penetration; the circular economy is moving significantly faster.

The infrastructure enabling this growth has matured considerably. Authentication technology, once the primary barrier to consumer trust in luxury resale, has improved dramatically through a combination of AI image analysis, blockchain provenance tracking, and third-party verification services. Platforms like The RealReal and Vestiaire Collective now operate with authentication rates and return policies that rival primary retail, removing the last significant friction points for mainstream adoption.

The Influencer Economy

The fashion influencer ecosystem has matured from a scrappy, semi-professional world of personal style bloggers into a highly structured, multi-billion dollar marketing channel with its own economics, hierarchies, and emerging regulatory frameworks. There are estimated to be between 15 and 20 million active fashion content creators globally in 2026, ranging from mega-influencers with tens of millions of followers to micro-creators with audiences in the low thousands, the latter increasingly prized by brands for their engagement rates and community authenticity.

The influencer marketing market in fashion is currently valued at approximately $11.1 billion and is growing at a compound annual growth rate of 32.9%, according to Influencer Marketing Hub. The mechanics of conversion have also changed fundamentally. Integrated commerce features — TikTok Shop, Instagram Checkout, Pinterest’s shoppable pins — have collapsed the traditional funnel between content discovery and purchase completion. Research from Bazaarvoice indicates that 49% of consumers now report making direct purchases through influencer posts at least occasionally, a figure that rises significantly among Gen Z consumers.

A newer and more philosophically interesting development is the rise of virtual AI influencers. Digital personas like Lil Miquela, Shudu, and a growing roster of brand-owned synthetic creators are attracting genuine engagement from younger audiences and in some cases, outperforming human influencers on specific brand metrics. These personas carry no personal controversies, are available around the clock, and can be deployed across multiple campaigns simultaneously. Whether they represent the future of fashion marketing or an uncanny valley curiosity remains genuinely contested.

FAQ

FAQ: The Questions the Industry Is Actually Asking

This section addresses the questions we hear most often from practitioners, investors, journalists, and informed consumers navigating the 2026 fashion landscape. The answers are deliberately direct and where the data is uncomfortable, we have not softened it.

How fast is the fashion technology market actually growing?

The fashion technology market, encompassing e-commerce infrastructure, AI trend forecasting, supply chain management software, virtual try-on tools, and circular economy platforms — is projected to grow from approximately $290.7 billion in 2026 to $485.8 billion by 2035. The primary engine of that growth is not AI design tools or augmented reality fitting rooms, as is often reported, but rather the more unglamorous category of circular economy logistics: the software and infrastructure needed to track, authenticate, resell, and reroute garments through multiple ownership cycles. That is where capital is flowing most aggressively.

Is the industry actually becoming sustainable or is that mostly marketing?

The honest answer is: both, simultaneously, in different parts of the industry. Fashion remains the second most polluting sector in the global economy, responsible for approximately 10% of annual carbon emissions and a disproportionate share of water consumption and microplastic pollution. The Ellen MacArthur Foundation estimates that less than 1% of clothing material is currently recycled into new clothing at the end of its life — a figure that has barely moved in a decade despite widespread corporate sustainability commitments.

At the same time, the circular economy infrastructure described elsewhere in this report represents genuine structural change, not mere marketing. Secondhand market growth, bio-material innovation, and the first serious regulatory pressure from the EU’s Extended Producer Responsibility legislation are beginning to alter the economics of throwaway fashion in measurable ways. The trajectory is positive but far too slow relative to the urgency of the environmental problem. The gap between corporate sustainability communications and supply chain reality remains one of the industry’s most consequential and unresolved tensions.

Why are brands still investing so little in technology?

The average fashion brand invests just 3–5% of revenue into digital transformation — strikingly low compared to financial services (10–15%) or automotive (6–8%). The reasons are structural rather than strategic. Fashion is an industry with deeply entrenched creative hierarchies where technology has historically been treated as a support function rather than a strategic driver. Design directors and CEOs who built their careers on intuition, taste, and relationships often lack both the vocabulary and the incentive to prioritise digital infrastructure. The investment case is also harder to make in an industry where brand equity — an intangible, hard-to-quantify asset — is often the primary value driver.

The consequence is an industry chronically underperforming its digital potential. AI tools that could dramatically reduce sampling waste, demand forecasting errors, and markdown rates sit underutilised in the technical departments of brands that continue to manage inventory through spreadsheets and gut instinct. The competitive pressure from data-native companies like Shein, which reinvests aggressively in algorithmic infrastructure, is beginning to shift this calculus — but the transformation is slow and uneven.

What is the ‘Phygital’ trend, and does it actually matter?

‘Phygital‘ — the convergence of physical and digital identity — is one of those industry terms that tends to provoke eye rolls in equal measure to genuine interest. The concept refers to the increasing blurring of the line between what consumers wear in physical spaces and what their digital avatars wear in virtual environments: gaming platforms, social media, the nascent metaverse infrastructure that continues to develop despite the post-2023 hype correction.

Whether it matters depends on your audience. For brands with strong Gen Z and Gen Alpha followings, digital fashion is a real and growing revenue channel. Fortnite skin collaborations with Balenciaga and Nike’s virtual product lines have generated tens of millions of dollars in digital-only revenues. The psychological logic is sound: brand identity formed in virtual spaces translates into purchase intent in physical ones. For brands targeting older demographics, the phygital opportunity is more distant, though the infrastructure is being built regardless of whether today’s primary consumers choose to use it.

What is driving the ‘quiet luxury’ trend, and how long will it last?

‘Quiet luxury’ — characterised by understated, logo-free, impeccably constructed garments in neutral palettes — is the aesthetic expression of a broader cultural anxiety about conspicuous consumption. Its rise corresponds neatly with post-pandemic economic uncertainty, a backlash against the maximalist streetwear aesthetic of the late 2010s, and the influence of critically acclaimed television like Succession, whose costume design became a cultural reference point for a certain aspirational sensibility.

Its commercial longevity is a genuine question. The labels that have benefited most — The Row, Loro Piana, Brunello Cucinelli, Jil Sander — were already building this aesthetic long before it acquired a name. For brands that pivoted toward ‘quiet luxury’ opportunistically in 2023–24, the shelf life may be shorter. Trend analysts at WGSN suggest the aesthetic will persist in some form through 2027–28, but will evolve toward what they term ‘craft luxury’: a renewed emphasis on visible artisanship and material provenance rather than simple restraint.

How is artificial intelligence actually being used in fashion right now?

AI’s current practical applications in fashion are less cinematic than the headlines suggest, but no less significant for that. The most commercially impactful uses are demand forecasting (reducing overproduction by predicting what will sell and in what quantities), personalised product recommendation engines (which drive a disproportionate share of e-commerce revenue), and dynamic pricing tools (which optimise markdown timing and depth to protect margin). These applications are well established at the large-platform level — Amazon, Zalando, and ASOS have deployed them for several years — but are only beginning to penetrate mid-size and independent brand operations.

On the creative side, generative AI tools are increasingly used in the early stages of design ideation — producing mood boards, colourway variations, and print concepts at speed. No major house has publicly deployed AI as a primary creative engine, and the industry’s creative directors are uniformly emphatic that human authorship remains central. The more interesting frontier is AI-assisted quality control and sustainability: computer vision systems that can inspect garments for defects at scale, and supply chain tools that use machine learning to map carbon exposure and labour risk across complex multi-tier supplier networks.

What does the near-term future look like for independent and emerging brands?

The conditions for independent fashion brands in 2026 are paradoxical: never has it been cheaper or easier to launch a brand, reach a global audience, and manufacture in small batches — and never has the competitive environment been more demanding. The democratisation of e-commerce infrastructure, social media distribution, and on-demand manufacturing has eliminated many of the traditional barriers to entry. At the same time, customer acquisition costs have risen sharply as digital advertising has become more expensive and algorithmic platforms have extracted more of the value from organic reach.

The independent brands navigating this environment most successfully tend to share a few characteristics: a clearly articulated and genuinely distinctive point of view, a community-first approach to audience development that prioritises depth of engagement over breadth of reach, and a supply chain built around transparency and craft quality that can support a premium price point. The era of the generic DTC label — a decent product, a clean website, and paid social acquisition — appears to be drawing to a close. What replaces it is something more demanding and more interesting: brand-building as genuine cultural production.

Final Takeaway: At the Edge of the Digital Cliff

The 2026 fashion industry is a $3 trillion ecosystem in genuine transition. Its creative energy has never been more distributed, emerging designers from Lagos, Seoul, and São Paulo are accessing global markets in ways that were structurally impossible a decade ago. Its sustainability crisis has never been more acute or more clearly understood. And its digital transformation, long delayed by cultural inertia and chronic underinvestment, is arriving in fragments: some parts of the industry moving rapidly, others barely having started.

The winners of the next decade will not be determined simply by who produces the most desirable product, though that still matters enormously. They will be determined by who masters the circular economy before regulation forces their hand, who builds the technological infrastructure to match their creative ambition, and who understands that in a world of infinite digital content and scarce human attention, the only truly defensible asset is a story that people want to be part of.

Fashion has always known how to tell stories. The question, in 2026, is whether it can also learn to build the systems that give those stories somewhere to go.

Sources:

- McKinsey & Company, The State of Fashion 2026

- Statista Global Fashion Market Outlook 2026

- Business of Fashion, The State of Fashion 2026: When the Rules Change

- International Labour Organization (2025), Decent Work Challenges and Opportunities in the Textiles and Clothing Sector

- Textile Exchange Materials Benchmark 2026 Reporting Essentials

- BoF & McKinsey (2025), The State of Fashion: Technology (Special Edition)

- Euromonitor Luxury and Fashion 2026, Digital Retail Index 2025

- 25/26 Fashion trends: Data analysis – WGSN

- Influencer Marketing Benchmark Report 2026

- WGSN | Trend Forecasting & Analytics 2025-2032

- eMarketer, Fashion Ecommerce 2026.

- LVMH Annual Report 2025

- Google Trends, Fashion Search Behaviour Analysis 2025

- Influencer Marketing Hub, The Benchmark Report 2026

- Hype Auditor, State of Influencer Marketing 2026.